On June 29, 2016, a new case was added to the growing list of evidence signaling the importance of redlining as a key area of focus for Fair Lending compliance. In a joint effort between the Consumer Finance Protection Bureau (CFPB) and the U.S. Department of Justice (DOJ), BancorpSouth was accused of several discriminatory practices related to redlining and other Fair Lending risk factors in its lending patterns from 2011 through 2013.

In a recent article – Evaluating Redlining Risk in Mortgage and Consumer Lending – ADI discussed the emerging trends in redlining compliance and how institutions, like BancorpSouth, can analyze their lending patterns for redlining risk, to understand and manage that risk before examiners come knocking.

In this article, we use the recent BancorpSouth case to walk through how public data, as are available in our proprietary data warehouse ADI Data ConnectSM, and various analytical tools and techniques can be leveraged to identify an institution’s exposure to redlining risk.

Screening for Markets with Redlining Risk

For institutions like BancorpSouth with activity dispersed across several markets, a critical early step in evaluating redlining risk is prioritizing the markets that show the greatest risk exposure. To help our clients, we developed a reporting tool – the Redlining SweepSM – to quickly identify and prioritize where mortgage lenders should focus their efforts to analyze exposure to redlining risk.

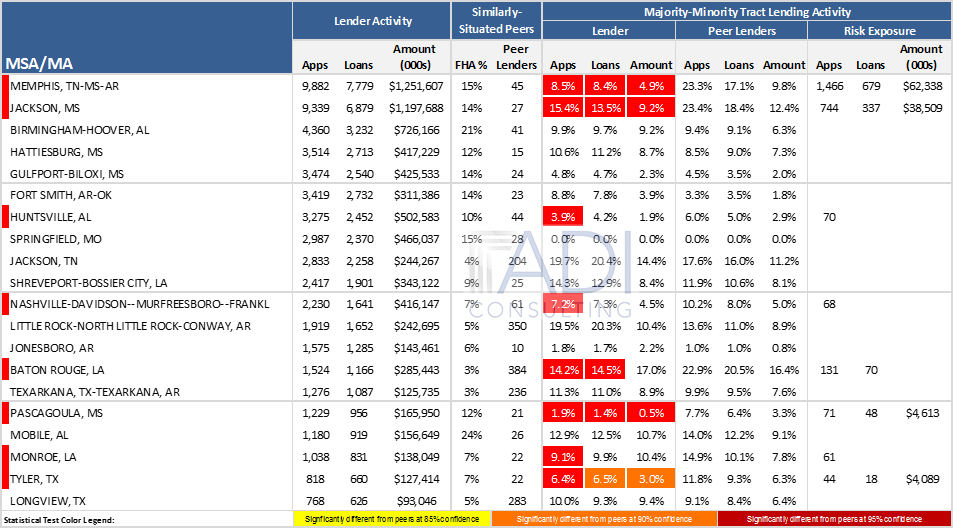

Figure 1. Redlining SweepSM of Top 20 Metropolitan Areas, BancorpSouth, 2011 – 2013

The results of the Redlining SweepSM for BancorpSouth, as presented in Figure 1, clearly show the market identified in the consent order – the Memphis, TN-MS-AR metropolitan statistical area (MSA) – as the most significant contributor of redlining risk to the institution. According to Home Mortgage Disclosure Act (HMDA) data, BancorpSouth needed an additional 1,466 applications from majority-minority census tracts in the Memphis MSA over the period of 2011-13 to match the distribution of the average similarly-situated peer in the market.

Evaluating Lending and Service Distribution within High-Risk Markets

Information provided in the Redlining SweepSM is helpful for identifying areas that require greater focus for redlining. But the story does not end there. While the Memphis TN-MS-AR MSA (Memphis MSA) is shown to be a primary driver of institutional redlining risk for BancorpSouth, we dug deeper to identify the intra-market drivers of the observed patterns.

Maps are a critical analytical tool when evaluating redlining risk. Figure 2 illustrates how a map can be used to identify the specific areas within the market that drove the observed patterns of market-level risk.

Figure 2. BancorpSouth Lending Penetration (2011-13) and Branch Distribution (12/31/13), Memphis MSA

The map highlights two critical issues within the Memphis MSA for BancorpSouth.First, relative to other areas, the bank was significantly less penetrated in majority-minority neighborhoods. The bank had an application penetration rate of 3.7 percent in census tracts that were not majority-minority. This figure compares unfavorably to a 1.3 percent application penetration rate in census tracts that were majority-minority.

Second, the geographic distribution of BancorpSouth branches were not representative of the distribution of majority-minority census tracts. While 43 percent of the census tracts within the Memphis MSA were majority-minority, only 22 percent of BancorpSouth’s branches, by the end of 2013, were located in majority-minority census tracts.

Both of these issues – poor penetration and lack of branches in majority-minority census tracts – were identified within the CFPB’s consent order. As the map shows, these issues were particularly acute within the inner city of Memphis, TN, where:

- BancorpSouth was less penetrated than in outlying majority-majority areas; and

- Branches tended to be located just outside the boundaries of clusters of majority-minority neighborhoods.

Using Models to Identify and Prioritize Risk

So far, we have analyzed public data to identify a potentially high risk market for redlining (i.e., the Memphis MSA) and have used mapping to show where that risk may be concentrated. Yet there may be additional factors that should be considered that can explain the observed patterns. We may find that after accounting for these factors – such as competitive intensity, real estate activity, product mix, homeownership levels and building types (e.g., single family homes, mobile homes, etc.) – the overall risk level may be lowered or even eliminated.

Regression models may be developed to control for these potentially explanatory variables. The outcome of this effort may provide a more precise assessment of risk and help prioritize the neighborhoods that offer the greatest realizable opportunity to lower redlining risk. Rather than having to consider all 159 majority-minority census tracts in the Memphis MSA, a well-designed modeling plan may pinpoint for BancorpSouth a small subset of specific areas where it can most effectively and efficiently:

- improve market penetration;

- open new branches; and,

- increase its marketing presence.

A Learning Opportunity for Banks and Mortgage Lenders

The BancorpSouth consent order is just the latest in a series of cases in recent months that show the increased focus regulatory agencies and the DOJ have on redlining issues. While other Fair Lending issues related to underwriting and pricing were identified in the consent order, the exclusion of branches and marketing activities from high-minority concentration areas and the exclusion of these areas from its assessment area under the Community Reinvestment Act were primary arguments in the CFPB’s complaint against BancorpSouth.

For other banks and mortgage lenders, the BancorpSouth case provides a great learning opportunity for incorporating redlining into their compliance management system. The complaint offers a new data point in understanding how the CFPB and other agencies screen lenders for redlining violations. The problematic lending patterns and branch distributions identified for BancorpSouth, Hudson City Savings, Associated Bank, etc. can be leveraged as benchmarks or other elements in an effective compliance monitoring system.

At ADI, we analyze these cases to refine our tools and techniques for identifying and managing Fair Lending risk, and we are reviewing this latest case for new insights that can be implemented in our client solutions. We encourage you to evaluate your compliance management system for any opportunities to identify and address the issues that BancorpSouth and others have encountered, before your examiners do.

Download the PDF HERE.